Choose a template

May 14, 2026

9 min read

Borrowing Money from Family and Friends for Your Business in 2026: How to Do It Right

Content

If the bank says “no” to your loan application, who will be the one you’ll ask for help? Parents, siblings, or close friends are the most common sources of support for small businesses when other funding sources fail. However, this deal can strengthen your connection just as easily as it can destroy it if not treated with due seriousness. So, what should you know about asking for a loan from a friend or a relative for your business needs?

Small business loans from friends and family are often considered a form of self-funding, or bootstrapping. You borrow money from a relative or friend to start your business, with a legal obligation to repay it under the terms stated in a family loan agreement. When taking this money, you must remember it is debt, not a gift, and should be treated like any other business loan.

This option is especially popular among small business owners because many startups do not qualify for bank financing. Nearly ¼ of small businesses applying for loans are denied financing and asked to provide collateral or personal guarantees, even when the business idea looks strong. In this case, a private loan is a faster, more flexible solution.

When you have no money to start a business, taking a required sum from your dear ones has many benefits, but it also comes with pitfalls. Here are the key ones:

Faster access to cash: You do not have to wait for weeks to get the money since there is no bank underwriting process.

Flexible terms: While the bank usually leaves no room for negotiation, the person you know may accept more favorable terms, such as a longer repayment period or interest-only payments.

Lower cost: Loans from banks and financial institutions may presuppose rather high effective rates, while private loans are usually more affordable.

Relationship-based trust: A friend or relative may lend money just because they know you, even if your business has a limited history.

Relationship risk: If you miss payments, it can create lasting tension with your lender and even destroy friendships.

Unclear expectations: If you decide to rely on handshake agreements rather than a solid promissory note and a repayment plan, you may find yourself in a situation where one party treats it as a loan, while the other treats it as “help.”

Tax problems: If you borrow money from a friend or relative, the IRS expects it to look like a real loan. If the interest rate is too low or there is no interest at all, the IRS may treat it as a gift, requiring extra paperwork.

Loss of independence: Some lenders, especially if they are your close people, may expect a say in your business decisions because their money is involved.

Collection issues: If the business fails, your lender will have to choose between enforcing the debt and preserving your relationship, which is a difficult decision.

Always start with a sincere conversation. Even if the lender is a close friend or someone you trust, they will want to understand how you plan to use the money and how you will repay it. If you feel uncomfortable at this stage, the loan itself may be a bad idea.

The first thing your lender wants to know before giving you the money is that you will repay it. Therefore, you should set a clear repayment schedule that your business can realistically meet. You can choose fixed monthly payments or a set term (for example, 24 to 60 months). If your revenue may vary by season, you can propose a flexible structure: smaller payments during slow months and larger payments during peak months.

A reliable payment plan should contain the information about:

The amount borrowed;

Interest rate (and whether it is fixed or variable) or additional charges;

Loan start date and final payoff date;

Payment frequency;

Payment method;

Late payment rules;

What happens after default;

Termination terms.

Also, decide whether the lender receives:

A personal guarantee from you;

Collateral (such as equipment);

A late-fee rule;

A prepayment option with no penalty.

While giving you their money, the borrower should be aware of all the pitfalls and risks they may face. Therefore, it is important to discuss what happens if:

The business fails, and you cannot repay on time.

Cash flow fluctuates, which causes late payments.

A dispute arises over whether the money was a loan or a gift.

The lender asks for the money back earlier due to a personal emergency.

The lender wants to influence your business decisions.

The business goes bankrupt, and the lender wants the right to that asset.

At this stage, the lender may either reject their offer or suggest certain changes in the payment plan to secure themselves.

The IRS generally treats properly structured borrowed money as a loan, not income, so you do not pay income tax just because you received loan proceeds. The key is that it must be documented as a real loan: written terms, a repayment obligation, and interest at or above AFR when required.

The interest rate is very important in family and friends loans. The IRS expects the lender to get at least the lowest rate, called the Applicable Federal Rate (AFR), under Internal Revenue Code §7872. AFR changes monthly and depends on the loan term (short-, mid-, or long-term). If you charge less than AFR, the IRS can impute interest, which creates tax consequences for both sides.

A loan from relatives can also be reclassified as a gift when facts show there was no real expectation of repayment. The IRS may suspect it if you have no:

Promissory note;

Repayment schedule;

Interest;

Payments made.

In this case, your family member or friend may need to file a gift tax Form 709 if the amount is over the yearly gift limit, and a no‑interest or low‑interest deal can also create extra IRS paperwork because the IRS may treat some interest as if it should have been paid.

So, the borrower does not report the loan to the IRS, but the lender must report the interest received from this loan as income.

If you want to protect both sides, document everything you agree on. Words do not work in business, even if you work with your friends or relatives. Here are the files both you and the lender should sign:

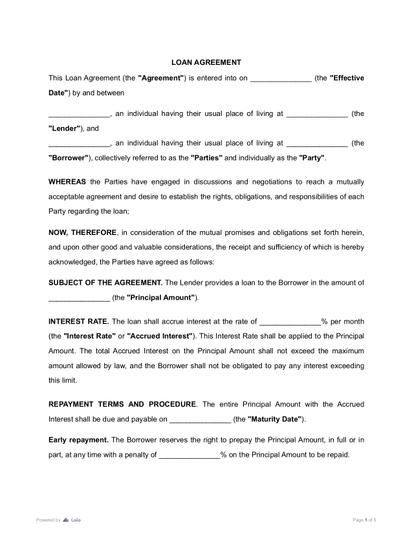

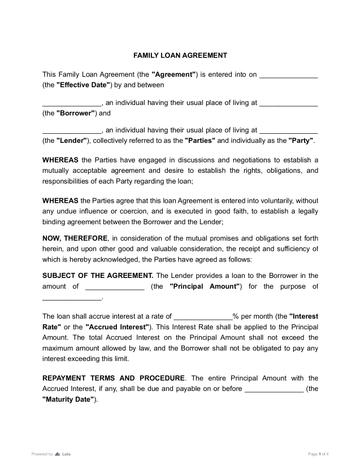

Promissory note: The basic legal IOU that states the amount borrowed, interest rate, payment schedule, due date, and what counts as default.

Loan agreement: A more detailed contract that adds practical rules, such as reporting requirements, late fees, prepayment terms, and what happens if the borrower violates the terms. Many small loans combine this with the promissory note.

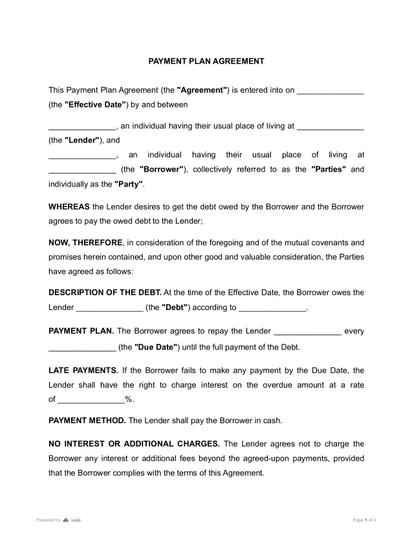

Repayment plan: It can be part of the promissory note or a separate document that clearly states when and in what amounts the payments will be made.

Security agreement (if collateral applies): Creates the lender’s right to take specified collateral (e.g., the borrower’s equipment, car, or real estate) if the business fails and the loan cannot be repaid.

UCC-1 financing statement (if collateral applies): A document that informs other creditors that the lender has a claim on the collateral. It helps the lender protect its priority rights if you later borrow from someone else.

Personal guarantee: This document provides a guarantee from a third party that the debt will be repaid even if the borrower fails to do so.

Each of these documents should be electronically signed by both the borrower and the lender (and any other parties involved) and kept until the debt is fully paid off and for 7 years after. In the event of any changes to the loan terms, the parties should either create a new document or amend the existing one.

Borrow based on your worst realistic month, not your best month. If your plan assumes “sales will ramp fast,” set payments at a level you can still handle if revenue comes in late or lower than expected.

Treat the loan like a bank would. Set a fixed payment date, use automatic transfers, and pay even when it feels awkward. Consistency protects the relationship.

Use a separate business account and pay business expenses from it. It makes it easy to prove where the money went and avoids the “Did you spend my money on personal stuff?” conversations.

Give simple updates on the payments. A short note once a month informing the lender that the payment has been made is enough.

Make a strict repayment plan. “I’ll pay you back when I can” causes stress. Use exact numbers and dates, and write them down.

If more than one person lends money, pick one point of contact. You do not want to explain the same issue to four relatives with different opinions. One person can share updates with the rest.

Start smaller and earn the right to borrow more. A first loan can cover a clear milestone (inventory for the first three months, initial marketing, a piece of equipment). If you hit targets and repay on time, a second loan becomes an easier “yes.”

Do not mix a loan with control. If your lender expects decision-making power, it is no longer a simple loan. Either keep it as debt with clear terms or consider an equity investment with separate documents.

Business loans from family members and friends can be a great source of early funding, but only if you treat it like a real loan. Clear terms, honest risk discussion, and proper documentation will protect everyone involved. When you respect both the relationship and the paperwork, you give your business and your personal ties the best chance to stay strong and flourishing.

July 24

12 min read

How to Read a Profit and Loss Statement

July 29

12 min read

How to Open a Business Bank Account for Your Company

March 27

9 min read

The Financial Documents Checklist for Small Businesses: 2026 Guide

July 24

10 min read

Grant vs. Loan: What's the Difference?

March 27

12 min read

How to Register a Company in the US: What No One Tells You in 2026

August 5

8 min read

What to Do When Client Refuses to Pay

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.