Choose a template

Updated March 17, 2026

10 min read

Independent Contractor Setup Checklist: Legal and Tax Rules for 2026

Content

If you are figuring out how to become an independent contractor, there are some things you should know before you start. Understanding the legal and tax setup is essential at the beginning. Many people searching for what do I need to be an independent contractor or how to become a 1099 contractor are really trying to avoid the same problems: tax surprises, payment disputes, unclear classification, or missing paperwork.

This guide explains how to work as an independent contractor in a legally structured way from the start. It covers worker classification, tax obligations, business licenses, and the contracts and records that help you get paid properly and stay compliant.

Under U.S. law, an independent contractor is defined not by job title, but by the nature of the working relationship. Contractors generally control how work is done, supply their own tools, and can work for multiple clients. Employees, by contrast, are economically dependent on the employer and subject to detailed direction.

This distinction affects taxes, labor protections, and liability. It also explains why classification errors create downstream issues with payroll taxes, overtime claims, and benefits.

At the federal level, worker classification is regulated by the United States Department of Labor, which enforces wage and hour laws using an economic-reality analysis.

At the federal level, worker classification is regulated by the Fair Labor Standards Act (FLSA) and enforced by the United States Department of Labor (DOL), which applies an economic reality analysis. As of the DOL’s 2024 Final Rule, worker status is evaluated under a six-factor economic reality test, which in plain terms asks whether the worker is truly running an independent business or is economically dependent on the company for work. Courts and regulators look at factors such as the permanence of the relationship and the nature and degree of control to make that determination.

Worker classification is one of the biggest risk areas for freelancers and gig workers because errors are often not detected early. These issues typically surface later, when contracts are already signed, taxes have been filed incorrectly, or a dispute arises. At that stage, correcting classification errors can be costly, time-consuming, and challenging to reverse.

According to the independent contractor statistics, about 11.9 million people worked as independent contractors as their primary job, underscoring how standard, and how regulated, this work model is.

People asking, what do I need to be an independent contractor, are usually trying to avoid mistakes that show up later: unpaid work, tax surprises, or compliance issues.

In practice, independent contractors need to be prepared in three areas before accepting paid work.

They must be legally able to operate and enter into contracts, which may include confirming work authorization, business registration, or licensing, depending on the state and industry.

They need a clear tax setup so income can be tracked, reported, and paid without confusion at filing time.

They need documentation that defines their services, pricing, and payment terms so expectations are set before work begins.

Skipping any of these steps increases risk. Contractors who start working without clear documentation often run into payment disputes, scope confusion, or delayed invoices. Those who ignore tax setup early are more likely to miss estimated payments, underreport income, or struggle to reconcile client payments at filing time.

The core requirements most independent contractors need to address are outlined below.

Written contracts matter because they turn informal expectations into enforceable terms. Without them, independent contractors are more exposed to payment disputes, changing scope, and disagreements about what was promised, delivered, or owed.

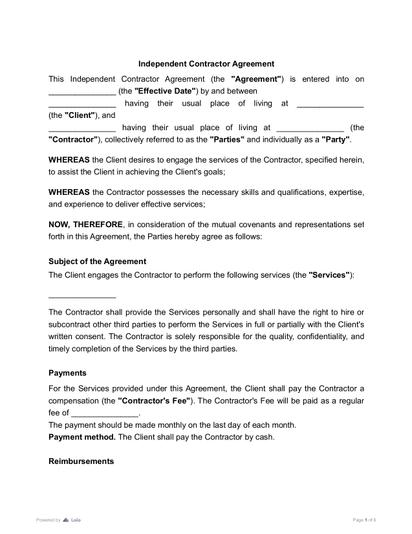

The foundation for most contractor relationships is an independent contractor agreement. This document defines the contractor’s status, outlines the scope of work, and explains how and when the relationship can end. It is especially important to clarify that the contractor is not an employee and to reduce classification risk.

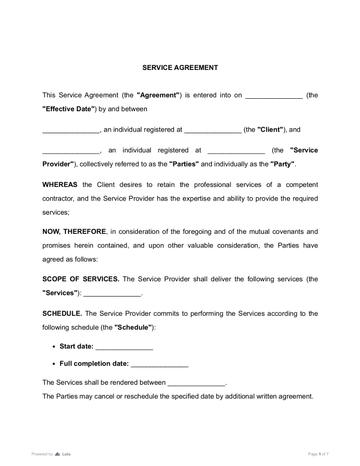

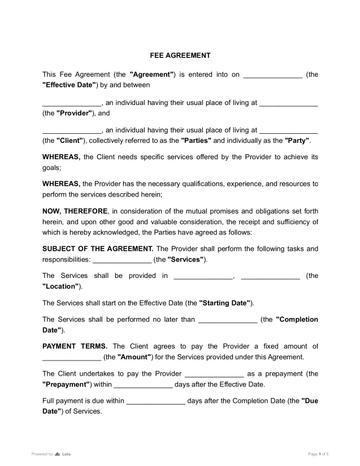

Beyond status and structure, the working details must also be defined. A service agreement explains what will be delivered, what the client is responsible for, and how performance will be measured. When payment terms are central to the engagement, a fee agreement sets the pricing model, billing method, and payment deadlines so compensation expectations are clear from the start. If payments will be made over time or delayed, a payment agreement documents installment arrangements and helps prevent disputes over timing.

These agreements should not only be signed but also stored and maintained in a structured way. Using an eSign solution helps document when agreements were executed and preserves an audit trail, while a built-in PDF editor makes it easier to adjust scope, pricing, or termination terms before finalizing the contract. Clean, version-controlled documentation reduces disputes later.

For solo contractors and small business owners, using structured legal templates can significantly reduce errors and inconsistencies. See reasons solo entrepreneurs and SMB owners should use legal templates for deeper insight.

Independent contractors are treated as self-employed for federal tax purposes. Instead of having taxes withheld from each payment, contractors are responsible for calculating, reporting, and paying their own taxes throughout the year.

At the federal level, the Internal Revenue Service treats contractor income as subject to both income tax and self-employment tax. This means contractors must track gross income, deduct eligible business expenses, and make estimated quarterly tax payments when required. These obligations apply regardless of whether a contractor works full-time, part-time, or in addition to other income.

For most independent contractors, federal tax compliance involves managing multiple obligations in parallel:

Income reporting. All contractor income must be reported, even if it was paid without withholding or received through multiple clients.

Self-employment tax. Contractors pay both the employee and employer portions of Social Security and Medicare through self-employment tax, calculated on net earnings.

Estimated quarterly payments. When taxes are not withheld at the source, contractors are generally expected to make quarterly estimated tax payments to avoid underpayment penalties.

Year-end reconciliation. Annual tax filings reconcile reported income, expenses, and payments made during the year.

Failing to file required returns or pay taxes on time can trigger compounding penalties and enforcement actions; see what happens if you don’t file taxes to understand the real consequences of noncompliance.

Setting aside money for taxes is only part of compliance. Accurate reporting depends on documentation that clearly supports every number filed. Independent contractors should maintain:

Invoices issued to clients. Shows who paid you, what services were provided, and when income was earned.

Contracts or statements of work. Explains the scope of services and supports why payments were received.

Deposit and payment records. Bank statements, payment processor reports, and deposit logs that confirm when income was received.

Expense records and receipts. Documentation for deductible business expenses, categorized consistently.

Income tracking logs. A running record that ties invoices, deposits, and totals together for reporting consistency.

IRS data and guidance show that underreported income and weak recordkeeping are major compliance risks for self-employed workers and sole proprietors. When reported income does not align with invoices, deposits, and third-party records, discrepancies are more likely to be flagged.

For independent contractors, good records do more than support filing. They help justify reported numbers, reduce review risk, and make year-end tax reporting much easier to manage.

Becoming a “1099 contractor” is less about status and more about how clients document payments. Two forms define this process: Form W-9 and Form 1099-NEC.

Clients typically request Form W-9 before issuing payment to capture the contractor’s legal name, business name (if any), tax classification, and taxpayer identification number. At this stage, the independent contractor completes Form W-9 as part of standard onboarding for 1099 work. This form supports year-end income reporting and allows the client to comply with IRS information-return requirements.

Providing accurate and consistent information on Form W-9 is essential. Mismatches between W-9 details and subsequent tax filings can trigger reporting discrepancies, leading to IRS notices, processing delays, or additional verification requests. Submitting correct information upfront helps ensure smoother income reporting and reduces administrative issues later.

When a client pays a contractor $600 or more in a year for services, the client generally reports those payments on Form 1099-NEC. Client reports nonemployee payments via Form 1099, which allows the IRS to match what the client paid with what the contractor reports as income. This form does not create tax liability on its own, but it serves as a cross-check between reported payments and the contractor’s tax return.

When contractor records do not align with 1099 totals, automated IRS systems may flag the return. Clean invoicing, consistent income logs, and accurate records are what prevent these issues.

Many contractors begin using their Social Security number, but an Employer Identification Number can be valid even when not strictly required. An EIN is commonly used when a contractor wants to avoid sharing an SSN on client forms, plans to scale the business, or hires employees.

Using an EIN also helps separate personal identity from business operations, especially when working with multiple clients or signing ongoing agreements. The IRS allows eligible individuals to obtain an EIN even as sole proprietors.

This is where documentation becomes essential. When contractors use a consistent business identity, pairing it with a written agreement helps align tax identity, service scope, and payment terms in one defensible record.

Whether independent contractors need a business license depends on where they operate and what type of work they do. There is no universal federal license that applies to independent contractors across all industries. Instead, licensing requirements are typically set at the state, county, or city level and vary widely by location and profession.

Many contractors assume that working independently or online means no license is required, but that is not always the case. Home-based contractors, freelancers, and consultants may still need to register locally, especially if they operate under a business name, advertise services, or receive payments tied to a specific location. Some industries also require professional or occupational licenses regardless of business size or structure.

In practice, independent contractors may need one or more of the following:

The FLSA sets standards for minimum wage and overtime pay, which apply to some kinds of workers, including employees but not independent contractors.

Independent contractors have different rights and responsibilities than employees, which are generally reserved for a union or state labor board to oversee rather than the Fair Labor Standards Act.

A general business license issued by a city or county.

A professional or occupational license for regulated fields (for example, construction, healthcare, real estate, or financial services).

A home-occupation permit is required if working from a residence.

A state-level registration is needed if operating under a trade name or collecting sales tax.

Licensing requirements are mandatory and are often enforced by local agencies rather than federal offices. The U.S. Small Business Administration recommends checking with state and municipal licensing authorities directly rather than assuming no license is required, as penalties typically apply retroactively once an issue is discovered.

Learning how to work as an independent contractor means learning how to invoice, collect payment, and document income consistently. Income tracking should begin with clear payment terms and continue through receipts, deposits, and records that tie back to signed agreements.

Invoices explain what was billed, receipts confirm payment, and agreements explain why the payment was owed. Using standardized templates makes this workflow easier to repeat and audit.

As your client base grows, managing documentation manually becomes risky. A secure PDF editor lets you update invoices and agreements without recreating documents from scratch, and integrated eSign functionality ensures legally binding payment terms arecaptured and stored. This structure makes income tracking easier and strengthens your position if questions arise.

Poor income tracking is one of the most common reasons independent contractors struggle with taxes and cash flow. Without consistent records of invoices, payments, and deposits, it becomes difficult to forecast income, plan expenses, or report earnings accurately.

March 27

12 min read

How to Register a Company in the US: What No One Tells You in 2026

July 24

12 min read

How to Start a Flooring Business and Get Your First Clients in 2026

July 22

8 min read

A Comprehensive Guide to Starting a Child Care Business

July 22

10 min read

Starting a Plumbing Business in 2026: What You Need to Know

July 7

10 min read

How to Start a Storage Unit Business

July 29

12 min read

LLC vs. Corporation: What to Choose for Your Business in 2026

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.