Choose a template

April 28, 2026

8 min read

Documents Required for a Business Loan: What You Need Before Applying

Content

Applying for a business loan can help companies fund expansion, manage cash flow, purchase equipment, or stabilize operations during slower periods. But before lenders approve financing, they need clear evidence that the business can repay the loan.

That’s why lenders ask for detailed documentation. These records help them verify your company’s legal status, financial health, and repayment capacity. Preparing the right documents in advance can significantly speed up the approval process and improve your chances of getting funded. Do you want to make the loan application process easier and improve your chances of approval? Take a few minutes to review the documents required for a business loan in this guide and prepare everything before you apply.

A business loan is a financing arrangement where a lender provides funds to a company with the expectation that the money will be repaid over time, usually with interest. A lender can be several types of financial institutions or organizations, including:

Banks — traditional commercial banks that offer business term loans, credit lines, and equipment financing.

Credit unions — member-owned financial institutions that may provide business lending with competitive rates.

Online lenders and fintech platforms — digital lending companies that often provide faster approvals and more flexible requirements.

Government-backed programs — such as loans supported by the U.S. Small Business Administration (SBA).

Private lenders or investors — individuals or investment firms that finance businesses directly.

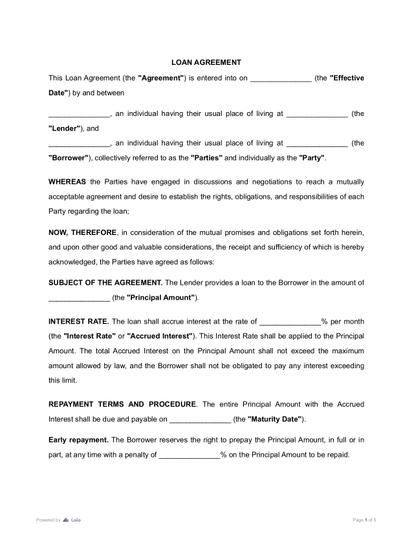

Once a loan is approved, the terms of the financing are usually documented in a loan agreement. A loan agreement is a legal contract between the lender and the borrower that outlines key details of the financing, such as the loan amount, interest rate, repayment schedule, fees, and any collateral required.

Businesses typically seek loans to cover operating expenses, purchase equipment or inventory, and hire employees. Many also use financing to expand into new markets and invest in growth opportunities. In fact, surveys show that the two most common reasons small businesses apply for financing are covering operating expenses (56%) and funding expansion or new opportunities (46%).

Before approving financing, lenders evaluate whether the business can responsibly manage and repay the loan. One of the most important tools in this evaluation is documentation. In practice, a business loan requires financial statements, tax records, and other documents that demonstrate the company’s financial stability.

Lenders are not only deciding whether to approve the loan — they are also evaluating how risky it is to lend money to your business. To make that decision, they review several aspects of your company, including its legal status, financial health, and the reliability of its owners. Most lenders follow a similar evaluation process. They want to confirm that the business:

Legally exists and operates in compliance with regulations;

Generates enough revenue to repay the loan;

Has responsible ownership and financial management;

Presents a reasonable use for the requested funds.

To assess these factors, lenders typically request documents that fall into three main categories:

Among all required materials, financial records are typically the most influential. A business loan requires financial statements because lenders depend on these documents to analyze profitability, debt levels, and cash flow stability. Even if a business has a strong idea or growth potential, lenders usually need clear financial evidence that the loan can be repaid.

Despite these requirements, many business owners hesitate to apply. Research shows that 44% of small businesses never apply for financing because they assume they will not qualify, even though they may meet lender requirements.

Documentation requirements vary depending on the lender and the type of financing. Once you have decided where you plan to apply for a loan — whether it is a bank, credit union, online lender, or government-backed program — the next step is to review the specific documentation requirements for that lender.

Banks tend to require detailed documentation, including several years of tax returns and full financial statements. Businesses can usually find the required document checklist on the bank’s official website, typically on the business lending or small business loan page. Many banks also provide downloadable application guides or checklists. If the requirements are not clearly listed online, loan officers or relationship managers at the bank can provide a document list during a preliminary consultation.

We reviewed 3 of the most well-known banks in the United States and identified their official loan application checklists and preparation guides:

Many alternative lenders request fewer documents and may focus on recent revenue or bank activity. Most online lender platforms automatically generate a document checklist after you start the application and enter basic business details, showing exactly what files need to be uploaded.

Loans backed by government programs often require additional paperwork because they follow stricter compliance guidelines. Businesses can find detailed document requirements on official government or program websites, such as the resource page provided by the SBA. These sites usually provide step-by-step application guides, required forms, and downloadable checklists explaining the documents applicants must prepare before applying through an approved lender.

Approval rates also differ between lender types. Smaller banks, for example, are often more flexible with qualified borrowers. Data shows that small banks approve about 83% of low-credit-risk applicants, compared with roughly 76% at large banks. Even with these differences, most lenders request similar core documents because they provide critical insight into a business’s financial stability.

Some financing products require less paperwork than traditional bank loans. These are often called low-documentation business loans or “low-doc” financing. They are designed for businesses that need quick access to funds or may not have the extensive financial history that banks typically require.

Common examples of low-documentation financing include:

Merchant cash advances

A lender provides funding in exchange for a portion of the business’s future credit card or debit card sales. Repayment usually occurs automatically through a percentage of daily transactions.

Short-term online business loans

Many online lenders offer short-term financing with simplified application requirements. These loans typically have repayment periods ranging from a few months to a couple of years.

Revenue-based financing

In this model, businesses receive funding and repay it through a fixed percentage of their monthly revenue until the agreed amount is repaid.

Instead of requesting full financial reports and multi-year tax records, lenders offering these products often rely on simplified documentation that reflects the business’s current cash flow and operational activity. For example, applicants may be asked to provide:

These documents allow lenders to quickly evaluate how much revenue the business generates and whether it can reasonably support loan repayments.

Low-documentation loans can provide faster access to funding, which makes them attractive for businesses that need immediate working capital. However, this convenience usually comes with trade-offs. Because lenders take on more risk when they rely on limited financial information, these loans often have higher interest rates, additional fees, or shorter repayment terms compared to conventional financing.

The exact documents required for business loan depend on the lender, but most applications include several core categories of documentation. Many of these required documents can also be found on document management platforms, which often provide libraries of business templates and forms that help companies prepare the necessary paperwork for financing applications.

If you want to understand which documents lenders typically request and how to prepare them correctly, continue reading to explore the full list of records commonly required for a business loan application.

Lenders almost always request tax returns when evaluating a loan application. These documents confirm reported revenue and provide an official record of the business’s financial history. Most lenders request business tax returns for the past two to three years and personal tax returns from the business owner.

In the United States, tax returns are filed using specific IRS forms, depending on the business structure:

IRS Form 1120 — Corporate Tax Return

Used by C corporations to report company income, expenses, and taxes owed. Lenders review it to evaluate the corporation’s profitability.

IRS Form 1120-S — S Corporation Tax Return

Filed by S corporations to report financial results that pass through to shareholders. It helps lenders understand the company’s performance.

IRS Form 1065 — Partnership Tax Return

This form is for the partnerships to report revenue and expenses. Each partner receives a Schedule K-1 showing their share of profits or losses.

Schedule C (Form 1040) — Profit or Loss From Business

Used by sole proprietors to report business income and expenses as part of their personal tax return.

Form 1040 — Individual Tax Return

Shows the business owner’s personal income and tax history, which lenders review when assessing creditworthiness.

These forms allow lenders to verify income and confirm that the financial information in the loan application matches official Internal Revenue Service filings.

A financial statement provides a detailed snapshot of a company’s financial condition. Because a business loan requires financial statements, lenders carefully analyze these reports before approving funding. The most common financial statements include:

Balance sheet

Shows assets, liabilities, and equity.

Income statement (profit and loss statement)

Shows revenue, expenses, and profitability.

Cash flow statement

Shows how money moves in and out of the business.

Before submitting your application, make sure the financial statements are recent, accurate, and consistent with your tax returns and bank records. Lenders often compare these documents to confirm that the reported numbers match.

For larger loans or startup financing, lenders often request a business plan. A business plan supports a business loan by explaining how the funds will be used and how the company expects to generate future revenue. A lender-focused business plan typically includes:

Business overview and operations;

Market and competitor analysis;

Revenue model;

Financial projections;

Loan purpose and repayment strategy.

Be specific about how the loan money will be spent (for example, equipment purchase, inventory, hiring staff, or marketing) and include realistic financial projections for the next 12–24 months. Clear numbers and practical use of funds help lenders understand how the loan will support business growth and repayment.

Some business loans require collateral, which is an asset the borrower promises to the lender as security for the loan. If the borrower cannot repay the loan, the lender may have the legal right to take and sell the asset to recover the unpaid balance. Loans backed by collateral are usually called secured loans.

Because collateral reduces the lender’s risk, lenders usually require documents that prove the asset exists, belongs to the borrower, and has enough value to support the loan amount. These records help the lender confirm that the asset could realistically be sold if repayment problems occur.

Typical collateral documentation includes:

For example, if equipment is used as collateral, lenders may review the purchase agreement. Before submitting this document, businesses can also review it themselves using an AI contract summary tool, which helps quickly identify essential clauses, ownership details, and any missing information that lenders may expect to see.

Another common requirement when applying for a business loan is the Employer Identification Number (EIN). The EIN is a unique identification number issued by the IRS that functions similarly to a Social Security number, but for businesses. It is used by government agencies, financial institutions, and tax authorities to identify a business entity.

Lenders rely on the EIN to verify important details about the company and confirm that the business is properly registered. When reviewing a loan application, lenders use the EIN to:

Verify the business identity and confirm the legal entity applying for the loan;

Access tax and financial records associated with the business;

Confirm regulatory and tax compliance with federal reporting requirements.

Providing the EIN allows the lender to match your application with official government records and confirm that the business operates as a legitimate legal entity.

If you want to learn more about how to obtain an EIN and register your company, you can read our detailed guide on how to register a business in the US, which explains the registration process and key identification requirements for new businesses.

Loans backed by the U.S. Small Business Administration (SBA) usually require more documentation than many other types of business financing. Because SBA loans are partially guaranteed by the federal government, lenders must follow strict verification and compliance procedures before approving funding. As a result, applicants are typically asked to provide detailed financial records and supporting documents that demonstrate the business’s financial stability, ownership structure, and ability to repay the loan.

Typical SBA loan documentation includes:

Business and personal tax returns;

Personal financial statements;

Detailed business financial statements;

Business licenses and registrations;

Ownership documents;

A comprehensive business plan.

Although the documentation process can be extensive, SBA loans remain popular because they often offer favorable interest rates and longer repayment terms. In fact, the SBA approved 58,000+ loans worth over $32 billion in a recent period, demonstrating its significant role in financing small businesses.

For businesses comparing options, the documents required for SME loan applications are often similar, but SBA-backed loans typically involve more detailed verification and stricter requirements in exchange for better terms.

If your company is structured as a limited liability company (LLC), lenders typically review both the business and the owners behind it. The approval process generally includes:

LLC owners are also commonly asked to provide their EIN. You can usually find your Employer Identification Number in:

IRS confirmation letters;

Business tax returns;

Payroll records;

Previous financial or loan documents.

Preparing the correct documentation is one of the most important steps when applying for financing. Lenders rely on records such as tax returns, financial statements, business plans, and collateral documentation to determine whether a business can responsibly repay a loan.

While requirements vary between lenders, most applications require similar core records that verify legal status, financial health, and operational strategy. By organizing the business loan documents before applying, business owners can reduce delays, present a stronger application, and significantly increase their chances of securing funding.

July 14

4 min read

Addendum vs Amendment: Change Your Purchase Agreement Properly

July 10

Sales Commission vs Bonus: What Is the Difference and How to Choose

July 23

13 min read

How to Buy an Existing Business in 2026: Step by Step Instructions

July 22

What is an Assignment of Contract? Transferring Rights and Duties Safely

June 12

8 min read

Statement of Work vs. Scope of Work: Strengthen Your Project

July 24

12 min read

How to Read a Profit and Loss Statement

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.