Choose a template

March 16, 2026

9 min read

The Financial Documents Checklist for Small Businesses: 2026 Guide

Content

Running a business means making constant decisions based on your financial reality. Pricing, hiring, borrowing, and growth all depend on a clear, reliable view of the business's current position.

Financial documents make that clarity possible. They show how money moves through the business, whether operations are sustainable, and what level of financial risk exists. When records are incomplete or poorly maintained, opportunities are missed, lenders hesitate, and compliance risks increase. These problems often become visible only when cash runs short, a loan is denied, or an audit begins.

Financial documents are records that track, report, and explain how money flows into, through, and out of a business. They include:

Formal financial statements.

Supporting records behind those numbers.

Signed documents, often completed with eSign, when approval or commitment must be documented.

Together, these documents help businesses:

Make decisions based on real financial data.

Prepare taxes and support compliance.

Plan cash needs and monitor risk.

Show credibility to lenders or investors.

Business owners rely on them to evaluate performance, forecast cash needs, prepare taxes, and verify reported numbers if those numbers are ever questioned.

Poor financial documentation creates real business risk. According to industry research, cash flow mismanagement accounts for approximately 82% of small business failures, underscoring how weak financial records can lead to serious operational problems.

Financial documents help owners make decisions based on real numbers, not guesswork. They show performance, cash flow, and risk, and they help businesses stay prepared for taxes, audits, and funding reviews.

In practice, they help businesses:

Forecast costs and revenue.

Adjust budgets.

Monitor cash flow.

Support loans and compliance.

Most small businesses rely on three core financial statements: the income statement, the balance sheet, and the cash flow statement. Together, they provide the clearest view of performance, financial position, and liquidity. Reporting expectations also depend on business structure, which is why formation choices and timelines matter, especially for new entities such as LLCs, where setup decisions can affect reporting obligations.

A balance sheet shows how a business’s resources are structured at a specific point in time. It lists assets, liabilities, and equity, allowing owners and stakeholders to see what the business owns, what it owes, and the remaining value attributable to the owner.

Assets typically include cash, accounts receivable, inventory, and equipment. Liabilities include loans, lines of credit, and accounts payable. The difference between assets and liabilities represents equity.

Balance sheet reports assets, helping stakeholders understand the business’s financial position at a glance.

The balance sheet is widely used by lenders, investors, and management to assess liquidity and solvency. It also provides essential context for decisions about borrowing, repayment, or reinvestment.

An income statement shows how revenue is generated, what expenses are incurred, and whether the business produces a net profit or loss over a defined period. Unlike the balance sheet, it focuses on performance rather than position.

An income statement summarizes revenue, making it easier to track trends over time, identify rising costs, or spot weakening margins. Business owners frequently rely on income statements to evaluate pricing strategies, control expenses, and demonstrate profitability in loan applications.

A cash flow statement shows where cash comes from and where it goes by categorizing activities as operating, investing, and financing. It answers a practical question that profit alone cannot: whether the business has enough cash to meet obligations.

Cash flow statement tracks cash, showing timing differences between revenue earned and cash received. This makes it indispensable for managing payroll, supplier payments, and short-term planning.

Cash flow problems remain one of the most common causes of business failure, underscoring the need to review this document regularly rather than only at year-end.

Supporting financial documents explain the activity behind your financial statements, including how revenue is earned, payments are collected, and obligations are recorded. Lenders, auditors, and business owners use them to verify accuracy and assess risk, and the Internal Revenue Service relies on the same records to validate reported income and deductions for tax compliance.

Supporting financial documents explain the real activity behind the numbers shown in financial statements. They help businesses verify revenue, track payment obligations, support tax reporting, and show lenders, auditors, or partners how specific transactions were handled in practice.

A tax return is the official form or set of forms a business files with the Internal Revenue Service to report income, deductions, credits, and tax liability for the year. U.S. business tax returns play an important role beyond internal reporting because lenders and investors often request them to confirm that reported revenue aligns with what was officially filed and to assess overall financial stability.

The exact return depends on business structure: sole proprietors generally report business income on Schedule C attached to Form 1040, partnerships file Form 1065, S corporations file Form 1120-S, and C corporations file Form 1120.

When reviewing a business tax return, lenders typically focus on gross receipts, taxable income, and related income figures because those sections help validate revenue, show expense structure, and provide an external benchmark against internal financial statements.

Reminder: The IRS generally requires businesses to keep supporting financial records for three years from the date a return is filed, and up to seven years in certain situations, such as when claiming a loss from worthless securities or bad debts. Keeping organized documentation protects you in the event of an audit or loan review.

Tax forms and supporting records are the paperwork behind the tax return. While the tax return is the formal filing submitted to the IRS, these records show how contractor payments, employee withholding, and other tax-reporting obligations were handled throughout the year.

A Form W-9 is typically collected from contractors and vendors to confirm taxpayer identification details before payments are made, so year-end reporting is accurate.

A Form W-4 is used when employees join, allowing them to set federal withholding so payroll calculations match the amounts that must be withheld and reported.

For nonemployee pay, a Form 1099-NEC is used to report compensation paid to independent contractors and is often reviewed when businesses need to support deductions and payment histories. And where sales tax applies, sales tax forms and exemption certificates document whether a transaction was taxable under state or local rules, which matters when records are audited or questioned later.

Keeping these forms complete and up to date helps ensure that figures reported on financial statements and tax filings stay consistent and defensible. It also reduces delays during audits, lender reviews, or government inquiries.

Failing to maintain or file required tax records can lead to escalating penalties and enforcement risks; if you want to understand the consequences in detail, see what happens if you don’t file taxes.

An accounts receivable aging report groups unpaid invoices by how long they have been outstanding, such as 0–30, 31–60, or 90+ days. This allows businesses to estimate near-term cash inflows and prioritize collections.

The best time to protect accounts receivable is before the invoice is issued — when payment terms are set in writing.

For companies that bill customers after delivery, aging reports are critical for avoiding cash shortages and planning operating expenses.

These reports depend on clear, consistent documentation, including invoices and payment terms.

Beyond tax records and receivables reporting, businesses also rely on operational financial documents that explain specific transactions, payment obligations, and incoming payments.

These documents are listed separately because they support the numbers in financial statements at the transaction level, showing how revenue was billed, how payment terms were structured, and how obligations were created or fulfilled.

Revenue starts with documentation that shows what was delivered, what was billed, and when payment is due. Invoices are the practical backbone here because they capture the billed amount, payment terms, and due date, which directly shape accounts receivable and cash flow timing. Receipts then close the loop by confirming that a payment was actually made or received, helping reconcile bank activity against open invoices and recorded income.

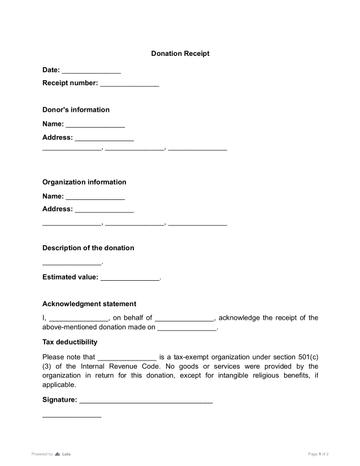

For day-to-day payments received in person, a cash receipt provides a clear record of the amount paid and when it was paid. When funds are collected for a specific purpose or event, a donation receipt documents the amount received and supports clean tracking and reporting.

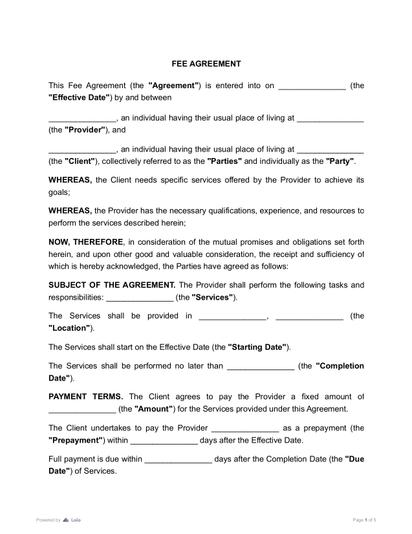

Not every client pays in a single transaction, and not every service has a simple, fixed price. When payments are made over time, payment agreements outline the schedule, installment structure, and what happens if a payment is missed, making collections easier and preventing misunderstandings. For service-based businesses, fee agreements document how services are billed, what fees apply, what is included, and when payment is due, reducing disputes over pricing or scope and supporting consistent revenue handling.

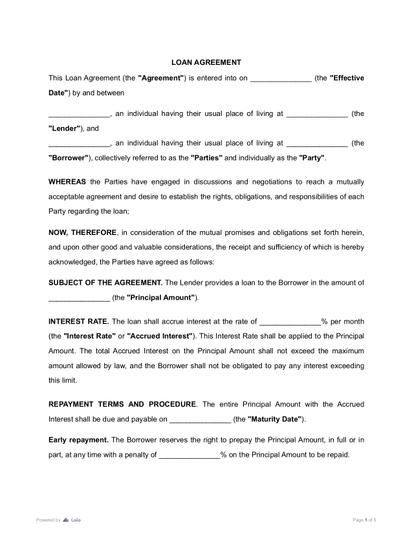

Liabilities should be explainable in plain documents, not just in accounting entries. Loan agreements provide the full structure behind borrowed funds, including principal amount, interest, repayment schedule, and default terms, which is why they are often reviewed during financing, audits, or partner diligence.

For simpler lending arrangements, promissory notes document the repayment obligation without a more complex loan package and help track outstanding balances over time.

Because these agreements directly affect long-term liabilities, understanding how to review a contract before signing is critical; see our guide on how to review a contract like a pro for practical review tips.

Together, these supporting financial documents keep financial statements defensible because they make every key number traceable to a real transaction, a real obligation, or a confirmed payment, exactly what lenders, partners, and auditors look for.

Effective financial document management starts with centralization. Records should be stored in a dedicated system rather than scattered across email inboxes or shared drives. Version control, clear naming conventions, permission-based access, and defined retention rules help prevent errors, duplication, and accidental data loss.

Many businesses rely on established platforms to manage this process. For example, QuickBooks is commonly used to generate invoices, track payments, and store transaction records in one place. Xero offers similar cloud-based accounting and document storage features, enabling teams and accountants to access real-time financial data securely.

For agreements and formal records, platforms like Loio combine eSign functionality with a built-in PDF editor, allowing businesses to prepare financial documents, adjust terms when needed, collect legally binding electronic signatures, and store finalized versions in a single secure location with a clear audit trail.

Using integrated systems like these helps businesses standardize financial paperwork, reduce manual errors, and keep every signed, updated document easy to retrieve during audits, financing reviews, or internal reporting.

July 24

12 min read

How to Read a Profit and Loss Statement

March 27

12 min read

How to Register a Company in the US: What No One Tells You in 2026

July 24

14 min read

How to Protect Your Small Business from Lawsuits

March 27

11 min read

The 2026 Tax Checklist: Every Federal Tax Your Business Has To Pay

July 30

15 min read

How to Manage Independent Contractors in 2026: The Compliance & Risk Guide

March 30

10 min read

How to Protect Intellectual Property Rights in 2026: A Legal & Digital Security Guide

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.