Choose a template

April 2, 2026

6 min read

Commercial Lease Termination in 2026: How to Get Out of a Business Lease Legally

Content

A commercial lease is one of the most rigid obligations a small business takes on. It does not adjust automatically when revenue drops, a location stops working, a partner exits, or the business shuts down. The lease is enforced through contract terms, notice mechanics, and remedies. That is why many “early exits” turn into expensive disputes: tenants leave the space without ending the obligation.

Commercial lease termination is rarely a single action. It is usually a process: you identify what the lease allows, you choose an exit route that actually changes your legal position, and you document each step so you do not trigger avoidable default while trying to leave.

Your lease ends according to the lease terms, not because you moved out, returned the keys, or closed the business. This distinction matters for anyone trying to understand how do I get out of a lease in a commercial setting, because the answer usually starts with the commercial lease agreement itself.

There are only a few clean exit routes:

Use an early termination clause (if the lease has one and you meet the conditions).

Transfer the lease through an allowed assignment or sublease (usually with landlord consent).

Sign a written surrender or termination agreement that clearly releases obligations.

If you “just leave,” it is usually abandonment, not termination. That pushes the dispute into the lease’s default and remedies section. State law can affect notice rules and damages, but the lease remains the primary rulebook controlling getting out of a commercial lease.

Unpaid rent during that period may be treated as arrears, triggering collection steps and damage claims. Understanding how rent arrears are handled in practice helps tenants gauge risk before stopping payments.

To get clarity fast, pull the documents that control the outcome: the signed lease, amendments, any personal guarantee, prior notices, and written side agreements.

For context, CBRE reported a 1.5 percentage point drop in downtown office vacancy since year-end 2024 (vs 0.5 points for prime suburban) and said retail’s overall availability rate held near a multi-year low in late 2025.

If you are looking for how to get out of a business lease, the key is choosing a route that produces a written release or a documented transfer. These are the real options for getting out of a lease without triggering enforcement.

You pay an agreed amount to exit the lease early under clearly defined terms, including the effective end date and mutual release of obligations. This is typically documented in a lease termination agreement, which specifies the buyout payment, confirms when rent and other charges stop, and reduces the risk of later disputes.

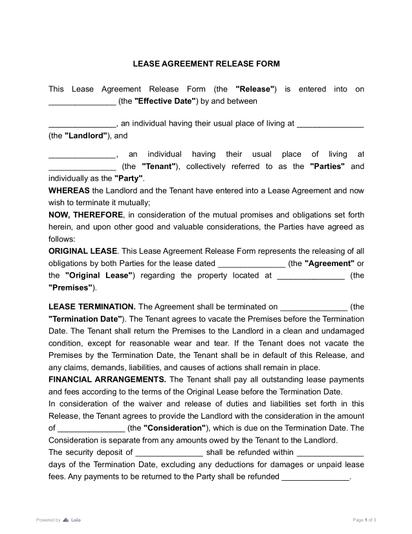

If the goal is a clean release from future claims, that language is often captured in a lease release agreement.

You transfer the lease to a new tenant, usually with landlord consent. Assignment does not automatically release you unless the consent clearly says it does.

A sublease can reduce cost, but you usually stay liable to the landlord. It’s a bridge unless paired with a release or converted to an assignment, and it’s typically documented in a commercial sublease agreement.

Subleasing can stabilize cash flow, but it requires strict compliance with consent, disclosure, and permitted-use clauses to avoid breaching the lease. The mechanics of legally subleasing commercial space explain how consent, notice, and liability layers interact.

Returning keys matters only if you sign a written surrender or termination agreement that sets the end date and the scope of release.

Temporary changes (deferral, abatement, sublease permission) can prevent default while you plan a transfer or surrender.

Bottom line: pick the route that ends obligations in writing, not the one that only gets you out of the space.

Start with the notice clause and deadlines. Then confirm default and cure rules, assignment or sublease permissions, and any early termination language. Read the personal guarantee as carefully as the lease.

Collect the key pages of the lease and amendments, rent ledger, condition photos or video, and major email or letter history. Include any default or late notices and any written term changes.

Use a PDF editor to merge the lease, amendments, notices, and condition photos into a single packet, and mark the clauses you’re relying on. Then pick the route you are actually pursuing: buyout, surrender, assignment, or sublease. If you need consent, prepare a replacement tenant package.

The tenant can send a written proposal with two or three structured options and a response timeline. Deliver it using the lease’s notice method to avoid disputes over “improper notice.” If you’re opening formal negotiations, sending a commercial lease termination letter can help clearly frame the request. It’s a simple formal written notice that outlines the requested exit terms and starts the negotiation in a clear, trackable way.

Get terms in writing. Focus on release scope, deposit handling, condition standard, restoration duties, fees, and final ledger timing. If there is a guarantee, confirm how the guarantor is released. Once terms are agreed, use eSign to execute the termination, release, or transfer documents, and store the signed copies in the final ledger.

When landlords dispute condition, mitigation, or consent requirements, the issue often becomes less about moving out and more about resolving landlord-tenant conflict under the lease terms.

Document the walkthrough, return keys and access, close utilities, and complete any required removal. Get written confirmation of the effective end date and final accounting.

Commercial lease exits are enforced through paperwork, not intent. These documents are what typically determine whether you actually got out of a lease or only moved out of a space.

Many leases set early-exit costs through fixed amounts or formulas, which is why this clause often becomes the focus once a tenant asks to leave early. In practice, the landlord claims liquidated damages when the lease defines a set fee or a rent-based calculation tied to the remaining term and re-leasing costs.

If your lease includes a liquidated-damages formula, the fee is calculated exactly as written. Suppose it does not, the “exit price” is usually negotiated around remaining term, re-leasing costs, and condition work. Mitigation rules vary by state, so don’t assume the landlord must mitigate damages the same way everywhere.

In limited cases, force majeure may excuse a breach of contract, but only where the clause clearly applies and the event falls within its scope.

Most problems occur when tenants try to get out of a commercial lease by taking action alone, rather than using the written procedures the lease requires.

Common mistakes to avoid:

Leaving without a signed release or transfer → get a written surrender/termination or assignment with release terms.

Missing notice rules or deadlines → follow the lease notice clause and keep proof of delivery.

Assuming key return ends the lease → keys are turnover, not termination, unless the agreement says so.

Stopping rent too early → check default and cure rules before changing payments.

Ignoring personal guarantee risk → review it early and negotiate guarantor release.

Default judgment or eviction record risk → unresolved disputes can affect future leasing and financing, and clearing records depends on outcome and state procedure.

Weak move-out documentation → take dated photos/video and request a documented walkthrough.

Treating a sublease as an exit → assume you remain liable unless released in writing.

Forgetting end charges (CAM/NNN, utilities, restoration) → ask for an interim ledger and set a final accounting deadline.

A commercial lease rarely ends cleanly on its own, so the safest approach is to treat termination as a documented process, not a moment. If you are asking how to get out of lease obligations early, the goal is to replace assumptions with written outcomes: a release, a defined end date, and a final accounting that closes the file. When you follow the notice rules, choose a real exit route, and keep strong records, you reduce costs, shorten disputes, and protect yourself from lingering liability.

April 9

10 min read

Buying vs. Leasing Commercial Property in 2026: Which Is Better for Your Business?

July 14

4 min read

Addendum vs Amendment: Change Your Purchase Agreement Properly

July 13

5 min read

Commercial Lease Negotiation & Mastering the Deal

May 24

9 min read

How to Buy Commercial Property in 2026: A Practical Guide

March 30

10 min read

Commercial Real Estate Leasing Process: 2026 Guide

May 21

12 min read

How to Sublease Your Office Space Legally: A Complete Guide for SMBs

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.