Choose a template

Updated March 30, 2026

10 min read

Commercial Real Estate Leasing Process: 2026 Guide

Content

Do you need to lease space and think it’s simple — find a place, agree on the price, sign, and move in? Renting a commercial space is a long-term commitment that affects your costs, flexibility, and future growth. With about 24% of U.S. offices sitting empty, tenants often have negotiation power. Still, the best spaces remain competitive. In this guide, we will explain, step by step, how to rent commercial space and show what truly matters before you sign.

A commercial lease is a legal agreement that allows a business to use property for business purposes. Unlike residential leases, commercial leases are designed to support profit-generating activity — offices, warehouses, retail spaces, restaurants, clinics, and more.

What makes commercial leases different is flexibility. Most terms are negotiable. In today’s market, flexibility is becoming a broader priority, with trends like “portfolio elasticity” gaining traction. At the same time, 72% of organizations still prioritize cost reduction according to JLL’s Top Global CRE Trends report.

A net lease is where the rent looks cheaper at first — and then the extra costs quietly show up. With this type of lease, some expenses that landlords usually cover are passed on to the tenant.

Here’s how it works, in plain terms:

Single net (N): You pay rent, and you also cover the property taxes.

Double net (NN): You pay rent, property taxes, and insurance.

Triple net (NNN): You pay rent, taxes, insurance, and maintenance — basically everything except the building’s name on the door.

Triple net leases are very common in retail and industrial spaces. The base rent is often lower, but the trade-off is responsibility. These leases work fine if you’re comfortable managing costs and planning ahead — just don’t assume “lower rent” means “lower total cost.”

A percentage lease means your rent doesn’t stop at a fixed number. You pay a base rent, and then a percentage of your sales — because when your business does well, the landlord wants to celebrate with you (financially).

Typical use cases:

Shopping malls;

High-traffic retail areas.

This setup can make sense in busy locations where foot traffic drives sales. It aligns the landlord’s interests with your success, but only works smoothly when sales tracking is accurate and transparent — otherwise, things get awkward fast.

A gross lease is the “no surprises, please” option. You pay one fixed rent amount, and the landlord handles most of the operating expenses behind the scenes.

Key features:

Predictable monthly costs;

The landlord covers property taxes, insurance, and maintenance;

Common in office buildings.

This type of lease is often chosen by smaller companies or growing teams that want simple budgeting and don’t want to track extra bills every month.

A modified gross lease sits between gross and net leases. Some expenses are included in rent, while others are shared or passed on after a set threshold.

You’ll usually see this setup in mixed-use or multi-tenant buildings, where dividing every bill perfectly just isn’t realistic.

Kate runs a small marketing studio and rents space in a building with several other businesses. Her lease includes basic operating costs in the rent, but if utilities spike or maintenance costs go beyond a set amount, tenants share the difference. Kate doesn’t have to manage every expense herself — she just keeps an eye on the line where “included” turns into “shared,” which feels fair enough for her stage of growth.

Not all commercial leases are created equal. While retail leases fall under the commercial leasing umbrella, they come with their own rules and priorities, especially when customer access and visibility matter.

Retail leases typically focus on:

General commercial leases usually allow:

A retail lease is usually the better fit if your business depends on:

Walk-in customers;

Storefront visibility;

Location-driven sales.

For service-based or back-office businesses, a standard commercial lease often provides better value.

Commercial leases usually last longer than residential ones, most commonly between 3 and 10 years, depending on the property type and market conditions. For business owners, the real question is how confident you are in your location and revenue over that period. A longer lease can secure better terms and stable costs, but it reduces flexibility if your needs change.

Short-term (1–3 years): Good for testing a location or business idea.

Mid-term (3–5 years): Common for small and growing businesses.

Long-term (7–10+ years): Often used by established companies seeking stability.

The right length depends on how predictable your business growth is and how easily you might need to relocate.

Here, we’ll walk through how to lease commercial real estate, showing what the process looks like for both tenants and landlords. You’ll see what usually happens, why each step matters, and what each side needs to think about along the way.

Whether you’re renting a commercial space for the first time or have done it before, it’s a good idea to review the key steps every tenant should know. Leasing is a structured process, and each stage, from defining your needs to signing the agreement, can impact your costs, flexibility, and day-to-day operations.

Start by defining your operational needs — determine the exact square footage, layout, customer access, parking requirements, and zoning compliance before touring properties. Avoid overestimating space, since unused square footage still increases rent and utility costs. Focus on locations that match how your business actually runs, not what simply looks impressive.

Use brokers, listing platforms, and local networks. Well-known platforms like LoopNet, Crexi, and CoStar can help you compare options for the commercial real estate leasing process in one place. Focus on properties that match your operational needs, not just your budget.

Look for "Class A" spaces. While they have higher face rents, landlords are currently offering record concessions — often 8% to 11% in rent discounts or "free rent" months — to attract stable tenants.

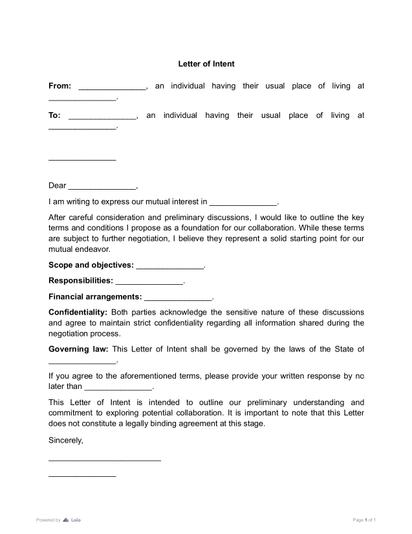

Once you identify a suitable space, the next step is to formalize your interest through a letter of intent (LOI). A LOI outlines the key terms of a commercial lease, such as rent, lease term, incentives, and responsibilities, before the full agreement is drafted. The tenant negotiates and submits the LOI to align with the landlord on the main terms early. It helps you gain clarity, reduce risks, and act as a checkpoint before committing to a legally binding lease.

Before focusing on rent, review the full structure of the lease. In commercial real estate, small clauses often cost more than headline price differences. Lease length, renewal rights, maintenance obligations, rent escalation formulas, personal guarantees, and exit options can affect your business for years.

According to the U.S. Bureau of Labor Statistics, lease structures often change over time. Among tenants who stay in the same space for more than five years, only 49.7% remain on fixed-term leases, while 50.3% switch to month-to-month agreements. This shift shows how important flexibility becomes in long-term occupancy. That’s why it’s essential to review lease terms carefully before signing — you’ll be bound by these conditions for the entire lease period.

Pay special attention to:

Lease term and renewal conditions;

Rent increases and escalation clauses;

Maintenance and repair responsibilities;

Early termination or sublease rights;

Personal guarantees.

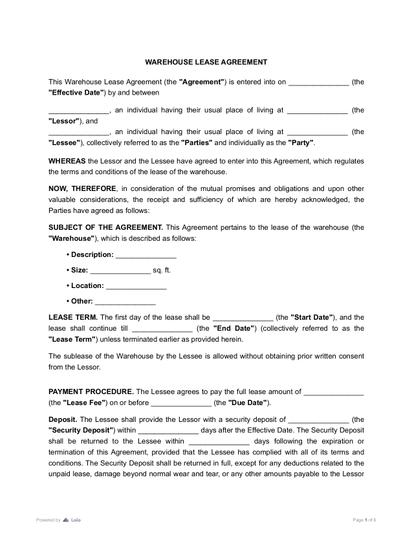

If you plan to lease industrial or storage space, you’ll typically sign a warehouse lease agreement – a commercial contract specifically designed for warehouse or industrial use, outlining rent terms, permitted storage activities, access rights, liability limits, and operational responsibilities. In this document, pay close attention to permitted use clauses, loading and access rights, ceiling height and power capacity, maintenance of docks and structural elements, insurance requirements, and liability for stored goods. Industrial leases often shift more operational risk to the tenant, so reviewing these provisions carefully can prevent costly surprises later.

Before signing, consider using an AI-powered contract review feature to reduce oversight risk. Simply upload your document into PDF Editor, and the AI contract review software instantly analyzes it. The tool extracts and highlights key contract elements — parties involved, purpose, dates, clauses, financial figures — and flags provisions that may require closer attention.

Commercial leases are expected to be negotiated. Rent, tenant improvements, free rent periods, and renewal rights are all fair points of discussion, and these terms are usually documented in a commercial lease agreement.

As a tenant entering a standard commercial lease, don’t rely solely on the landlord’s assurances. Verify that your specific business activity is legally permitted in the space — not just “retail” or “office” in general, but your exact use. Request written confirmation if necessary.

Inspect the condition of core systems such as HVAC, plumbing, electrical capacity, and internet infrastructure. If repairs are needed, clarify in writing who pays and when the work will be completed. Review the building’s certificate of occupancy and ensure there are no pending code violations that could delay operations. Finally, estimate your real move-in costs — build-out, signage, security deposits, insurance requirements, and potential upgrades.

Once terms are clear and agreed upon, sign and retain organized copies. Digital signing tools can make this step easier, especially for remote collaboration. Use a reliable platform that complies with the Electronic Signatures in Global and National Commerce Act (E-SIGN Act) and the Uniform Electronic Transactions Act (UETA). Under these laws, e-signatures carry the same legal weight as handwritten signatures — as long as all parties.

Start by confirming the property meets local building codes, fire safety standards, and accessibility requirements. You can verify these through your city or county building department, local fire marshal’s office, or the municipality’s official website, where building codes and inspection requirements are usually published. If needed, request a formal inspection or compliance confirmation before listing. Resolve any outstanding repairs before marketing the space — HVAC problems, plumbing leaks, roof issues, damaged flooring, or poor lighting.

Organize key documentation in advance, including the certificate of occupancy, recent maintenance records, zoning confirmation, and utility capacity details. Being prepared speeds up negotiations and builds tenant confidence. Clearly outline what operating costs are included in rent and who is responsible for maintenance, taxes, and common area expenses. Transparency reduces future disputes.

Before move-in, take detailed photos and videos of the space — walls, ceilings, floors, fixtures, and any existing damage. This creates objective evidence of the property’s condition in case disputes arise over repairs or security deposits later. Store the files securely and consider signing a move-in condition report with the tenant so both parties agree on the starting condition of the premises.

Relying on a “For Lease” sign alone limits exposure. List the space where serious tenants actually search. In addition to popular platforms, don’t forget to list your property on local commercial brokerage websites, as many regional businesses search there first when looking for space.

You should also publish listings on state or city business portals, where entrepreneurs often check available properties before opening or relocating a business. For niche spaces, consider posting in targeted Facebook or industry-specific groups, where you can reach qualified tenants directly within your target sector.

When creating the listing, accuracy and clarity matter more than marketing language. Tenants are comparing numbers and risk, not adjectives. Describe the space clearly:

Exact square footage (rentable and usable, if applicable);

Lease type (gross, NNN, modified gross);

Base rent and estimated total occupancy cost;

Permitted use and zoning;

Ceiling height, power capacity, loading access (for industrial);

Foot traffic and visibility (for retail);

Parking availability and access points;

Build-out condition (shell, turnkey, second-generation);

Lease term flexibility.

2,500 sq ft Class B office space located on the 3rd floor of a multi-tenant building. Gross lease at $28/sq ft annually, including property taxes and common area maintenance. Open layout with 3 private offices, conference room, kitchenette, and reception area. On-site parking (15 spaces), elevator access, and high-speed fiber internet available. Zoned for general office use. 3–5 year lease term with renewal option. Move-in ready condition.

Use professional photos with natural lighting and wide angles. Include a simple floor plan if possible. Avoid exaggeration — experienced tenants will verify details during due diligence, and inconsistencies reduce trust. Clear, detailed listings attract more qualified tenants and reduce time spent answering repetitive questions.

When you rent out commercial space, careful tenant screening protects your long-term income. Review the tenant’s business history, financial stability, and ability to support the lease term. Request financial statements, references, and proof of funds where appropriate. Confirm their intended use complies with zoning and won’t create issues with other tenants. For newer businesses, consider a personal guarantee and a risk-adjusted security deposit.

All commercial leases are different. The agreement should reflect the type of space and how it will actually be used. Below is a comparison of two completely different spaces — office space and storage space — and how their lease terms should be drafted accordingly.

An office lease focuses on operational functionality and shared building responsibilities. It typically defines rent structure, lease term, renewal options, maintenance duties, permitted use, signage rights, parking, access hours, and common area expenses. Because office tenants rely on utilities, HVAC, internet capacity, and daily occupancy, service levels and repair timelines should be clearly addressed. Tenant improvements and flexibility clauses are often key negotiation points.

A storage space lease, in contrast, centers on access control and liability limitation. The agreement should clearly define permitted and prohibited items (especially hazardous materials), access hours, security measures, insurance requirements, and limits of landlord liability for stored property. Maintenance obligations are usually simpler, but risk-control clauses are stricter. Unlike office leases, build-outs and operational flexibility are rarely central issues.

Landlords don’t need to draft these documents from scratch. Many use contract management platforms that offer libraries of ready-to-use commercial lease templates, which can then be customized to fit the specific property and tenant.

Adjust terms to attract quality tenants while protecting your interests. Instead of lowering rent immediately, consider offering structured incentives like a short rent-free period, tenant improvement allowance, or phased rent increases in exchange for a longer lease term or stronger deposit.

Clarify maintenance responsibilities, cost-sharing, and escalation terms upfront, and document every concession in writing. A balanced lease protects your cash flow while keeping the property competitive in the market.

Once signed, manage the lease actively through clear communication and regular compliance checks. Staying organized with rent schedules, maintenance responsibilities, and renewal dates prevents misunderstandings and keeps the landlord-tenant relationship running smoothly.

Using Loio’s contract library helps you store and easily retrieve lease agreements, ensuring that renewal terms are always accessible for manual review before the deadline passes.

You’re unlikely to run into problems with a commercial lease if you understand the process and the terms before signing. But if you’re worried about making a costly mistake, or you’ve already seen how things can go wrong, it’s worth learning from the most common pitfalls others face.

The most important thing to remember is that there is no such thing as a "standard" lease; almost every line is up for negotiation. Landlords usually present a draft that heavily favors their interests, so it is up to you to push back and ensure the terms are balanced.

To lease or to buy? The right choice depends on how stable your plans are and how much commitment you’re ready to take on. Leasing commercial property makes sense when you want:

Lower upfront costs;

More flexibility to relocate or scale;

Less responsibility for long-term property management;

A safer option while testing a location or business model.

Buying commercial property works better when you want:

Full control over the space;

Long-term stability in one location;

Equity instead of ongoing rent payments;

Confidence that the property fits long-term plans.

Many companies lease first and consider buying later, once revenue is stable and the location is clearly proven.

If you decide to buy instead of lease, clear paperwork is still essential. A commercial real estate purchase agreement is commonly used to document the purchase price, closing terms, timelines, and responsibilities of both the buyer and the seller.

A commercial lease is rarely a “set it and forget it” document. In practice, many long-term leases are amended at least once during their term — often because business needs change faster than the original agreement anticipated. A lease isn’t always static. Updates are common when:

The business expands or downsizes;

Ownership structure changes;

New regulations apply;

Renewal periods approach.

Amendments help keep the lease aligned with how the business actually operates.

The commercial lease process isn’t just about finding a tenant or a space and signing papers — even if it sometimes looks that simple. For both tenants and landlords, a little patience, clear communication, and a solid understanding of the lease terms can prevent costly misunderstandings later. Take the time to review responsibilities, risks, and long-term expectations carefully. The best lease is the one that still makes sense for both sides after the initial excitement wears off.

July 28

14 min read

Equipment Leasing Guide: How It Works and How to Save Money in 2026

May 21

12 min read

How to Sublease Your Office Space Legally: A Complete Guide for SMBs

March 27

12 min read

How to Register a Company in the US: What No One Tells You in 2026

July 21

4 min read

What Is a Fixed-Term Lease, and How Is It Different From an Automatic Renewal Lease?

July 14

4 min read

Addendum vs Amendment: Change Your Purchase Agreement Properly

July 24

12 min read

How to Read a Profit and Loss Statement

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.