Choose a template

Updated February 20, 2026

14 min read

How to Build a Sales Process: A 2026 Legal Guide

Content

Businesses sell something all the time — from the goods they produce to equipment that is no longer in use. Whether it is a one-time sale or a repetitive action, the entire process should be organized in accordance with all legal requirements. Otherwise, you might face legal issues, missed payments, or confusion with buyers. This guide explains how to build a sales process — from the list of documents to gather to how to get payments safely.

First, let's figure out what a sales process is. Two notions can help us with it: the sales funnel and the sales pipeline. Though related, they serve different purposes in helping you close more successful deals.

The sales funnel shows the stages a potential customer goes through before they make a purchase. Why is it a funnel? Because many clients will start the sales journey, but only some reach the bottom and actually buy.

A sales funnel includes several stages:

Awareness: The buyer first learns about your product or service through an ad, a visit to your shop or website.

Interest: The buyer wants to know more about the product.

Consideration: The buyer compares your offer with others.

Intent: They show serious interest: ask for a demo, negotiate price, or discuss terms.

Purchase: The deal is closed, and the product is sold.

The funnel helps you understand what a potential client needs at every stage. Someone who just learns about your product doesn't need a price sheet yet. Someone ready to purchase does.

The sales pipeline is a tool you, as a seller, need to track each deal's status day to day. Each pipeline stage reflects actions you take to move the buyer forward:

Prospecting: Search for potential buyers. Look for companies or individuals who might benefit from your product based on their industry, size, or current needs.

Lead qualification: Decide if the lead is a good fit. Check if they have a real need, buying power, and a budget that matches your offer.

Initial contact: Reach out to the lead by phone, email, or message. The goal is to introduce your product and start a conversation.

Defining prospect needs: Ask questions to understand what the buyer is looking for, their timeline, and any specific requirements.

Making an offer: Deliver a formal offer with product details, pricing, delivery terms, and other conditions.

Negotiation: Discuss terms, handle questions, and make adjustments if needed to meet the buyer's expectations.

Closing: Both parties agree to the deal. Contracts are signed, and payment and delivery terms are confirmed.

Delivery: Make sure the purchase reaches the client on time and undamaged.

So, the funnel shows the buyer's journey, and the pipeline is your roadmap to support and finish that journey. By understanding both, you can plan better, foresee revenue more accurately, and focus on the deals most likely to close.

Whatever you sell, you need documents to prove you have the right to do it. No reasonable buyer will proceed with the deal unless they get a guarantee that the new purchase won't cause them trouble.

So, to ensure the sales process will be fast and smooth, prepare these documents in advance:

Ownership documents confirm that you have the legal right to sell the goods. Without them, the buyer might suspect fraud, and you could run into legal issues. These records are also important for fast asset transfer and official registration:

Purchase invoices or receipts must include the seller’s name, the buyer’s name, date of purchase, product description, quantity, total cost, and method of payment. A scanned digital copy is acceptable, but keep the original file.

Title forms are on the list of essential documents when you sell vehicles or large equipment. The title should include the identification (VIN or serial number), the legal owner's name, and any lien information.

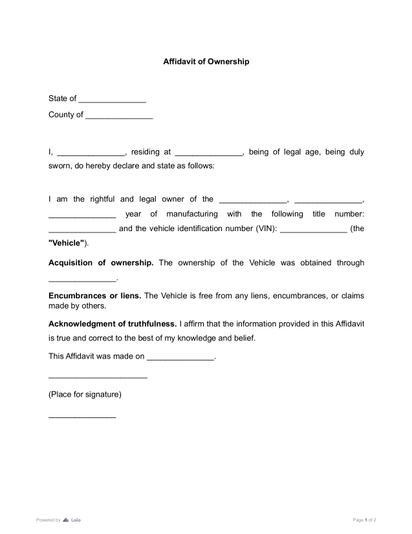

An affidavit of ownership is provided by the seller if the original ownership documents are lost.

The first thing you need to do is to show the potential buyer what they are going to purchase. A clear set of inventory documents helps close the deal faster and ensures your client won't have any claims after it:

Itemized inventory list: Include the names of items sold, their type, condition (new, used, refurbished), size, and quantity.

High-quality photos: Show all angles and include close-ups of defects or signs of use to improve the sales process.

Serial numbers: If it's a piece of equipment, device, or any other item that has a unique identifier, prepare the documents to confirm its authenticity.

Inventory tracking sheet: Note where the item is located, who the current owner is, and what status it has (available, on hold, sold) so that you do not sell one thing twice by chance.

To show that the items you sell meet safety and quality requirements, you need to provide corresponding certificates.

Safety certificates: They prove your product meets industry or national safety standards. In the U.S., you may need a UL (Underwriters Laboratories) certificate for electronics or machinery, an NSF certification for food-related equipment, or an ASME stamp for pressure vessels. The document should show who performed the test, when, what standards were used, and the results.

Warranty statements: If you're offering a warranty, whether from you or passed on from a manufacturer, put it in writing. State how long the warranty lasts, what it covers (parts, labor, or both), and how the customer can file a claim.

Official registration: Before sale, medical devices must be registered with the FDA, commercial vehicles or large construction machinery — tracked by VIN and listed with your state's Department of Motor Vehicles or similar authority. The document should contain the information about the agency issuing the registration, registration number, and validity period or expiration date.

Prospecting — identifying your client — is the first one of the sales pipeline stages. Once you have something to sell, you need to find the buyer. For this, you need to know:

Who needs this item;

What industry are they in;

What their typical budget is.

For example, if you sell farm tools, your main clients may include local farmers, suppliers, or agricultural co-ops. Their needs and purchase habits will be very different from those of clients in industrial or retail sectors.

Setting the price is an exquisite art: too high — and you push customers away; too low — and you lose profit. Therefore, the best way to determine the cost of your item is to rely on one of the following methods:

Cost-based pricing: Calculate your total cost (including labor, storage, and additional expenses), then add a markup to meet the sum you want to make.

Market-based pricing: Check what your direct competitors charge for similar products. Use tools like Google Shopping, industry-specific platforms, or B2B marketplaces (e.g., Thomasnet) to compare.

Value-based pricing: Consider how much your product is worth to the buyer — what problem it solves, how it improves efficiency, or how much it saves them long term. For instance, if your equipment cuts labor hours by 30%, it may justify a higher price.

Other factors that impact pricing:

Demand trends: Prices tend to rise during peak season or supply shortages.

Product age: New or upgraded models usually cost more; for older items, buyers may ask for a discount.

Condition: The price for new, refurbished, or used goods will differ greatly.

Depending on the state you live in, taxes and fees may vary. However, you should add these sums to your price if you do not want to pay them out of your own pocket.

Here are the most common taxes in the United States:

Sales tax: Varies by state and ranges from 4% to over 10%; some cities also add a local rate.

Excise tax: Applies to goods like fuel, alcohol, and heavy trucks, often due to their environmental impact or regulatory status:

Business income tax: Set aside enough to cover federal (21% for corporations) and state (up to 11.5%) tax obligations based on your business structure.

Where you sell is just as important as what you sell. The right channel increases your reach, simplifies logistics, and helps you meet your buyers' expectations.

According to the B2B Market and Customer Experience Report, in 2025, U.S. businesses had a 13% increase in online B2B sales.

Online selling lets you reach more buyers 24/7, including those in other states and countries. It's cost-effective and makes it easier to track inventory, automate payments, and gather customer data.

Offline channels, though less visible, remain important for trading products, especially those that require in-person inspection or demonstration, such as vehicles, machinery, or expensive tools.

Retail stores: Local businesses that display items for walk-in or call-in customers.

Trade fairs: Industry events where serious buyers come ready to make deals or source suppliers.

Direct sales: Sales reps visit businesses or call prospects with personalized offers.

Distributors or resellers: You provide the goods, and they handle local sales and support.

This is the stage where lead qualification, initial contact with the customer, and the analysis of the client’s needs take place. Potential customers react to your offer and, depending on it, you adjust the latter and choose those who are the most likely to make the next step — the actual purchase.

You can boost this process by using various outreach activities like emails, calls, or online ads. They will ensure you get your clients anyway, even if some refuse to make a purchase at some point.

If you manage many sales simultaneously, especially online, the use of CRM tools can be helpful. They allow you to make the whole process of interaction with the client centralized: track each deal by stage, follow up on time, and keep communication clear. Popular programs include:

HubSpot CRM;

Zoho CRM;

Salesforce;

Pipedrive.

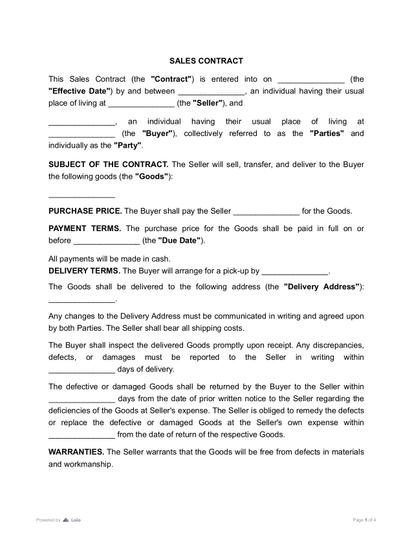

In business, a handshake isn't enough. Every sale, no matter big or small, should be registered in writing so that the interests of you and the buyer are protected and both of you have legal proof of the deal.

A sales contract is a legally binding document that spells out the terms, dates, responsibilities of the buyer and the seller, and the cost of the transaction.

A well-written agreement should include:

Buyer and seller details:

Product description:

Price and payment terms:

Delivery terms:

Warranties:

Dispute resolution:

Both parties’ e-signatures and the date.

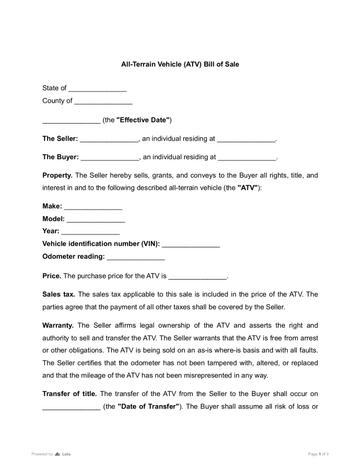

Though the sales contract is a universal document that can be applied to most deals, for some items, you may need a specific type of contract:

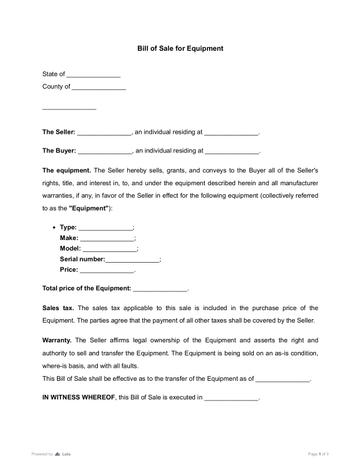

Consider using special templates if you sell equipment or heavy machinery, like an all-terrain vehicle (ATV) or a tractor.

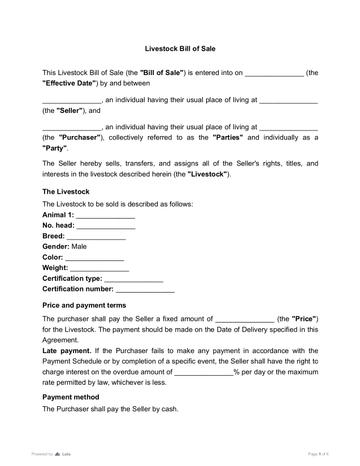

If you have a farming business and trade livestock, your document must contain the list of animals and essential details about each individual, like the breed, gender, color, certification type and number. The same rules, plus the information about a veterinarian examination, are applicable when you sell a horse.

You do not need to draft the sales agreement from scratch every time you sell something. Instead, use a reliable contract management platform, choose the required template, fill it in with all the necessary information, edit the document, and add e-signatures of the seller and the buyer. In such a way, you get a legally-binding contract in a few minutes, without the need to hire a lawyer.

Keep both digital and printed copies of your sales contract for at least 3–7 years after the deal, as required by IRS documentation rules in your state.

Delivery is the final stage of the sales pipeline. Once the contract is signed, your responsibility is to transfer the purchase to the buyer safely and on time. Delays or damages can destroy your business reputation and even lead to legal claims. Here is what you need to do:

Choose a reliable freight carrier or logistics provider: Research companies that have good reviews and check if they can handle your type of goods, especially for heavy, fragile, or regulated items. Request proof of insurance.

Confirm insurance coverage: Make sure the freight provider or you (the seller) have insurance that covers accidental loss, theft, or damage during transit.

Use proper packaging: Pack the item in accordance with the relevant industry standards for your product type. If it is an electrical, medical, or hazardous item, U.S. law requires special containers and warning labels.

Label items clearly: Include product name, quantity, SKU or serial number, safety warnings, and country of origin. For international shipments, label in English and the language of the buyer's country (if required).

Document the delivery: Include a packing list and a delivery receipt. Have the buyer or their representative sign the delivery note or bill of lading to confirm safe receipt.

The quality and reliability of your delivery service directly affect customer satisfaction and determine whether a buyer will choose to work with you again. Stay in regular contact with the customer until they receive their order, and always follow up after the sale with a thank-you message and a request for feedback. This not only shows professionalism but also helps build trust and long-term loyalty.

The buyer gets the purchase, and you get the money. To make sure the transaction goes smoothly and does not get blocked by the bank, it's important to choose the right payment method. Here are the most reliable options:

Bank transfer (ACH or wire): Best for B2B and large transactions. In the U.S., ACH payments usually take 1-3 business days.

Letter of credit: Often used for international deals. A bank guarantees payment after the buyer receives goods under agreed terms.

Online payment platforms (PayPal, Stripe): Easy to use for small-to-medium transactions. Processing fees are typically 2.9% + a fixed fee.

Credit/debit card: Ideal for online stores or retail orders. Use a PCI-compliant system to protect cardholder data.

Cash: Acceptable only for local, in-person deals. Always provide a detailed receipt and keep records of the transaction for tax purposes.

Whatever you sell, one small mistake can result in lost revenue and legal claims. To ensure the sales process brings you no trouble, do not make such mistakes:

Lacking proof of ownership.

Always keep receipts, invoices, or title documents. If you can't prove the goods legally belong to you, the buyer may pull out.

Skipping a written agreement.

A written contract protects both parties, outlining the terms, pricing, delivery, and guarantees. In the U.S., most states require written contracts for sales over $500 under the Uniform Commercial Code (UCC).

Not including taxes in pricing.

Each state has different rules and thresholds for taxable sales, especially for online or interstate transactions.

Using unreliable delivery services.

Work with trusted freight companies, especially when you transport high-value or heavy items.

Not verifying the buyer.

Always confirm the company's full legal name, tax ID, and purchase authority before shipping large orders or extending credit.

A well-organized sale makes the deal comfortable and beneficial for both the seller and the buyer. It includes many elements, from proper documents to safe payment. The sales process steps provided in this guide will help you to set each of them quickly and sell your goods the right way — legally, clearly, and with complete records. Every sale counts. Every detail counts.

March 27

12 min read

How to Register a Company in the US: What No One Tells You in 2026

July 24

12 min read

How to Read a Profit and Loss Statement

July 24

14 min read

How to Protect Your Small Business from Lawsuits

July 28

14 min read

Equipment Leasing Guide: How It Works and How to Save Money in 2026

March 27

11 min read

The 2026 Tax Checklist: Every Federal Tax Your Business Has To Pay

March 30

10 min read

Commercial Real Estate Leasing Process: 2026 Guide

Tweak agreements before signing or sending for signatures. Update details, add or remove clauses, adjust formatting, and redline changes instantly.

Sign documents and collect legally binding signatures. Invite up to ten people to sign in any order, track the progress, and send reminders.

Invite up to ten people to sign your document in any order. Get a finalized, audit-ready copy without chasing signatures.